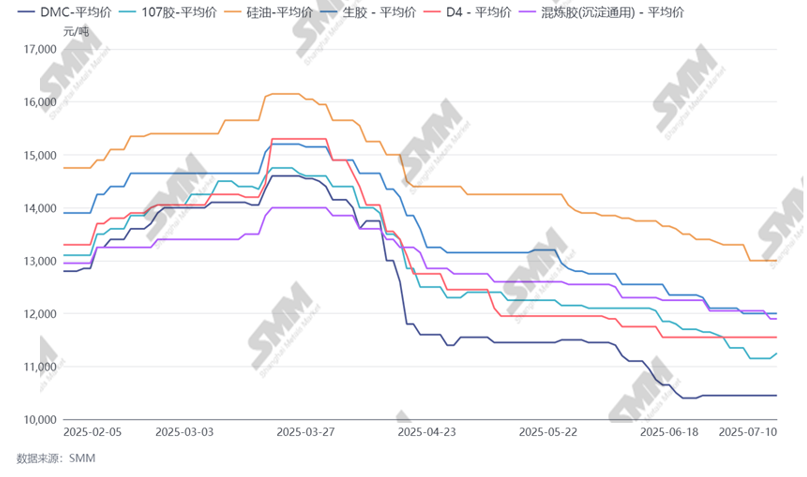

SMM reported on July 10: According to SMM, the bottom price of DMC in China this week was slightly raised to 10,700 yuan/mt, with monomer enterprises in east China quoting 10,700 yuan/mt this week, up 400 yuan/mt WoW. Other monomer enterprises raised their quotes to around 11,000 yuan/mt. Driven by this, the prices of various downstream DMC products are expected to increase slightly in the near future.

Figure: Price Trend of Silicone Products

SMM analyzed that the main reason for this price increase was the support from the cost side. Recently, the price of silicon metal has been continuously rising, with the average price of #421 silicon (used in silicone) in east China being 10,000 yuan/mt, maintaining stability this week. The average price of #421 silicon in east China was 9,100 yuan/mt, with a price increase of 100 yuan/mt this week. Both futures and spot prices of silicon metal have been strong recently, with the low price rising nearly 1,000 yuan/mt from the end of June. The costs of monomer enterprises have increased significantly. In addition, after the just-in-time procurement by downstream enterprises in the early stage, the inventory pressure of monomer enterprises has remained relatively stable. Driven by the cost support, the quotes have been raised.

Regarding the subsequent price outlook, SMM believes that the short-term DMC price is expected to remain relatively stable, oscillating around 11,000 yuan/mt. The main reasons are that it is currently still the traditional off-season for silicone, with poor end-use demand. Downstream enterprises mainly make just-in-time procurement. Especially since downstream enterprises have already made procurements in June, their current raw material inventories have not been fully consumed yet, and they are more cautious about this price increase. In addition, the recent price increase of silicon metal has also faced certain resistance, with the recent increase starting to slow down, and the cost support remaining stable. Therefore, it is expected that the subsequent DMC price will still show a fluctuating trend.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)